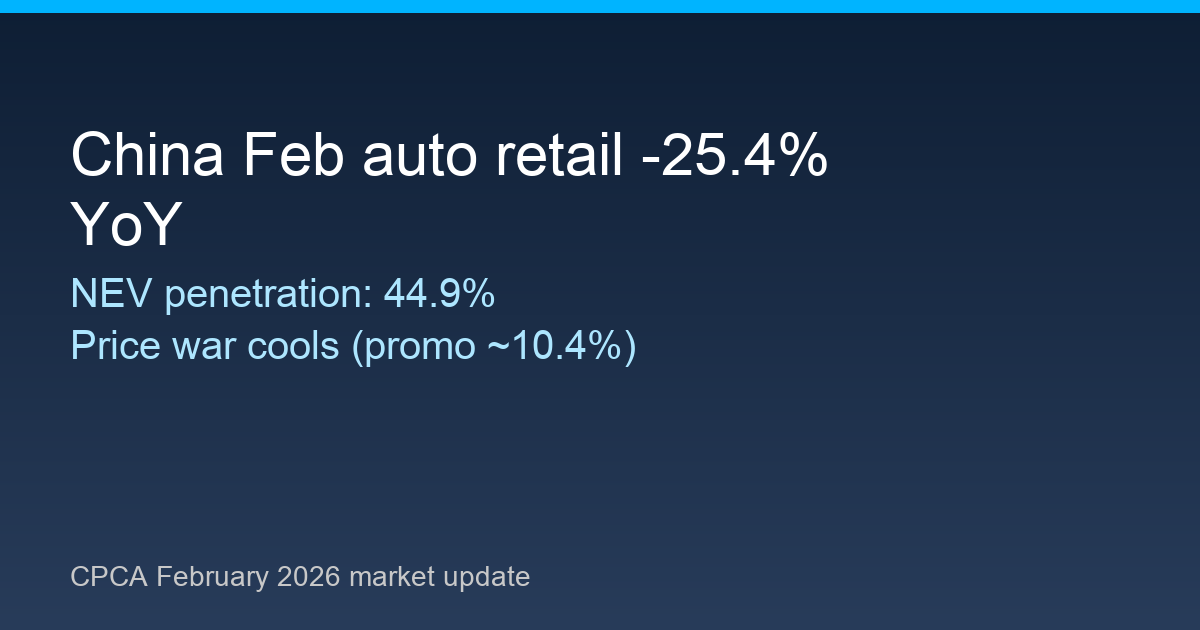

China’s passenger‑car market pulled back in February, but electrification stayed resilient. In its March 12 monthly analysis, the China Passenger Car Association (CPCA, a unit of the China Automobile Dealers Association) said February retail sales fell to 1.034 million units, down 25.4% year over year and 33.1% month over month. New‑energy vehicles (NEVs) accounted for 464,000 of those sales, a 32% annual drop, yet the NEV penetration rate still held at 44.9%. The same report noted promotion intensity around 10.4%, a sign that the price war has cooled as policy shifts, including the end of purchase‑tax exemptions, reset demand and inventory behavior.

The headline decline in February retail sales is sharp in both year‑on‑year and sequential terms, but the start‑of‑year totals show the market is still sizable. CPCA reported cumulative passenger‑car retail of 2.578 million units in January–February, down 18.9% from a year earlier. That two‑month total provides a clearer read on demand than a single month, and it frames February’s slump as part of a broader early‑year reset rather than a one‑off anomaly.

NEVs remain the core of the market even when volumes soften. CPCA’s data show February NEV retail at 464,000 units, with January–February cumulative NEV retail at 1.06 million units, down 25.7% year over year. The penetration rate of 44.9% means nearly one in two passenger cars sold was electrified, which signals that electrification is entrenched even when total demand is down.

Pricing dynamics offer an additional signal. CPCA said the NEV promotion rate was about 10.4% in February and has stayed near 10% for six straight months. That is a lower‑intensity discount environment compared with the most aggressive phases of the price war, and it suggests automakers are trying to protect margins rather than chase volume at any cost.

Policy context helps explain the more rational pricing stance. The CPCA analysis frames February demand against the backdrop of the purchase‑tax exemption ending and government calls to curb “involution” style, self‑defeating competition. With subsidies and tax benefits stepping back, automakers have less incentive to trigger a new round of deep cuts, and the industry appears to be testing whether demand can stabilize without heavy discounting.

The report also pointed to shifts in export structure and in the mix of domestic NEV brands, which matters for how the market recovers. A changing export mix can pull supply away from domestic retail, while brand‑mix changes often indicate which players are gaining pricing power in a calmer competitive environment. Even without detailed figures, the CPCA’s emphasis on structure suggests the next phase of competition will be shaped by product positioning and overseas channels rather than only by price, with new models such as VW–XPeng’s co‑developed EVs highlighting the shift.

Upstream battery data add another layer to the demand story. Industry figures cited by Chinese media show February power and energy‑storage battery sales at 113.2 GWh, down 23.9% month over month but up 25.7% year over year, with power‑battery sales at 74.5 GWh. The monthly dip lines up with the retail slowdown, yet the annual growth in battery shipments implies that production capacity and longer‑term electrification demand are still expanding. That contrast between monthly softness and annual growth highlights how supply chains are scaling even as retail demand oscillates.

Taken together, the February numbers paint a market in transition. The combination of a 44.9% NEV penetration rate and a promotion rate around 10% implies that consumers are still buying electrified models, but automakers are less willing to subsidize every sale. For global readers, the key takeaway is that China’s EV market is moving from a volume‑first phase to a period where product cycles, brand strength, and export competitiveness could matter more than blanket discounting.

What changed in February is that retail volumes fell sharply while price‑war intensity stayed muted, creating a split between demand softness and stable penetration. What may happen next is a gradual recovery in spring as new models and export demand absorb inventory, with March data likely to show whether the industry can rebuild momentum without reopening the discount spiral. If penetration continues to hover in the mid‑40% range while promotions stay low, China’s EV market could enter a more sustainable, margin‑aware growth phase.

Sources

- https://www.cada.cn/Trends/info_91_10455.html

- https://finance.sina.com.cn/roll/2026-03-12/doc-inhqtkar4849347.shtml

- https://www.yicai.com/brief/103083123.html

- https://finance.sina.com.cn/tech/digi/2026-03-12/doc-inhqtqkp4776888.shtml