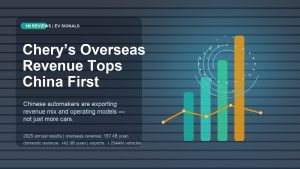

Leapmotor said in a Hong Kong exchange filing on March 16, 2026 that it delivered its first full‑year profit in 2025, a key milestone for China’s EV startups. The company reported net profit of RMB 5.4 billion on revenue of RMB 64.73 billion, up 101.3% year‑on‑year, after a RMB 2.82 billion loss in 2024, and several outlets said its annual sales roughly doubled. The result makes Leapmotor the second Chinese EV startup after Li Auto to reach annual profitability, signaling that scale and cost control are starting to reshape the country’s crowded EV market.

The numbers show a classic turnaround pattern: rapid revenue expansion and a decisive swing in bottom‑line performance. Leapmotor’s 2025 revenue of RMB 64.73 billion more than doubled from the prior year, and the company shifted from a loss of RMB 2.82 billion to a profit of RMB 5.4 billion. Those figures, disclosed in the Hong Kong exchange announcement and echoed by domestic financial media, are substantial in a sector where many startups still burn cash to gain share. For a young automaker, clearing the annual‑profit threshold is more than a symbolic milestone—it reduces financing pressure and suggests that the business model can survive outside of capital‑market support.

Sales growth was a direct driver of that profitability. CnEVPost reported that Leapmotor’s annual sales doubled in 2025, and the company’s own results indicate that scale was the key lever. In China’s EV market, where price competition has intensified, doubling unit deliveries in a single year is one of the few ways to spread R&D and manufacturing costs without sacrificing product development. The sales jump helps explain why Leapmotor could move from red ink to profit even as peers continued to discount aggressively.

Leapmotor’s achievement is also notable for what it says about the broader EV startup cohort. In the same reporting cycle, analysts and local media pointed out that Leapmotor is only the second new‑energy startup in China to become profitable on a full‑year basis, following Li Auto. That comparison matters because it highlights the bar that the market is now setting: profitability is increasingly becoming the gatekeeper for survival, not just a nice‑to‑have milestone. For investors and supply‑chain partners, the fact that only a handful of young EV makers can sustain profits underscores how the market is likely to consolidate around players with scale and manufacturing efficiency.

The industry backdrop makes the result even more consequential. The China Association of Automobile Manufacturers (CAAM) reported that new‑energy vehicle sales in China reached 16.49 million units in 2025, a massive market that continues to expand but is also crowded with both legacy OEMs and startups. In a market of that size, being able to grow sales fast enough to offset price pressure is difficult, and profitability becomes a stronger signal of competitive resilience. Leapmotor’s 2025 profit therefore serves as a proof point that some startups can still win despite the scale of competition and the rapid commoditization of EV hardware.

Financially, the magnitude of Leapmotor’s turnaround suggests more than a one‑off boost. A swing of more than RMB 8 billion between 2024 and 2025 implies a combination of higher volume, improved product mix, and tighter cost control, even though the company has not disclosed all of those details in the public brief. The revenue jump to RMB 64.73 billion and the shift to a positive profit base are strong signals that the business is leaving the “burn to grow” phase. That is particularly important in China, where EV price wars have squeezed margins across the sector and made profitability a rare achievement.

The outcome also raises strategic questions for 2026. If Leapmotor can sustain profitability, it gains flexibility to invest in new platforms, expand its dealer network, and manage pricing without relying solely on external capital. At the same time, maintaining profits in China’s EV market will require continuous volume growth or efficiency gains. The company’s current results show that scale is possible, but it still needs to prove that scale can be durable when competition intensifies and when new entrants with state‑backed resources continue to pressure pricing.

From a broader perspective, Leapmotor’s milestone could accelerate the market’s shift toward quality over quantity. In a year when NEV sales hit 16.49 million units, the challenge is no longer consumer acceptance of EVs—it is the sustainability of business models. Full‑year profitability signals that at least some Chinese startups are moving into a mature phase of competition, where operational discipline and manufacturing efficiency matter as much as product design. For policy makers and investors, that is a sign that the market is entering a new stage: fewer weak players, more emphasis on capital efficiency, and a higher bar for survival.

What changed is that Leapmotor’s 2025 results demonstrate that profitability is now achievable for an independent Chinese EV startup, not just for the largest incumbents. The next question is whether this is the start of a broader pattern or a narrow exception. If more startups cannot cross the profitability line soon, the sector is likely to see faster consolidation, tighter supplier terms, and stronger pressure to differentiate beyond pricing. Leapmotor has shown that the path exists; the market will decide how many can follow it.

Sources

- Hong Kong Stock Exchange filing — https://www1.hkexnews.hk/listedco/listconews/sehk/2026/0316/2026031601214.pdf

- Cailian Press (CLS) — https://www.cls.cn/detail/2314373

- Sina Finance — https://finance.sina.cn/stock/jdts/2026-03-16/detail-inhrevap8739209.d.html

- CnEVPost — https://cnevpost.com/2026/03/16/leapmotor-posts-1st-annual-profit/

- China Association of Automobile Manufacturers (CAAM) — http://www.caam.org.cn/chn/3/cate_38/con_5236999.html